Meaningful Progress

There has been meaningful progress on the inflation front. The annual rate of inflation has slowed, and the ever-visible price of gasoline is well off last year’s high. But as every child has asked on a long road trip, “Are we there yet?”

In other words, are we at or near the Fed’s 2% annual inflation target? Are rate hikes over? The short answer is no. Fed officials are still talking about higher interest rates and are touting the idea that it’s too soon to be discussing rate cuts.

Their fear is simple: declare victory too soon and a resurgence in inflation may ensue.

Let’s quickly review the numbers from last week’s Consumer Price Index (CPI), which was released by the U.S. Bureau of Labor Statistics.

The CPI slowed from 7.1% annually in November to 6.5% in December, matching expectations, according to CNBC.

The core CPI, which excludes food and energy, slowed from an annual rate of 6.0% in November to 5.7% in December, also in line with expectations.

On a monthly basis, the CPI fell 0.1% in December, matching expectations, as food rose 0.3% and energy fell 4.5%. The core CPI rose 0.3%, matching expectations.

The monthly CPI has come in below the core CPI in 5 of the last 6 months amid the drop in energy. That’s encouraging. We’re also seeing some moderation in core inflation, too.

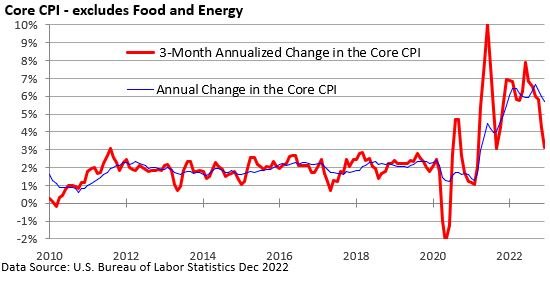

Let’s review the graphic below, which illustrates the annual change in the core CPI (blue line) and contrasts it with the 3-month annualized rate in core inflation (red line). The same gauge is being used, but the two metrics are calculated in different ways, providing different perspectives.

The annual rate is backward-looking and less volatile. The 3-month annual rate is more forward-looking. It’s quicker to pick up on trends, but it’s noisier and can give false signals.

At 3.1%, the 3-month annual rate has fallen dramatically from a recent June high of 7.9%.

Including food and energy, the 3-month annualized CPI was 1.8% in December.

Going forward, progress may be uneven. We may get some encouraging inflation numbers and some setbacks. But recent market gains suggest investors are on board with the idea that the rate of inflation is receding.

For now, the Fed appears set to slow its pace of rate increases, but it’s not fully satisfied with the current level of inflation, as it remains well above its 2% annual goal.

If you have any questions or would like to discuss any other matters, please let me know.

Clark S. Bellin, CIMA®, CPWA®, CEPA

President & Financial Advisor, Bellwether Wealth

402-476-8844 cbellin@bellww.com

All items discussed in this report are for informational purposes only, are not advice of any kind, and are not intended as a solicitation to buy, hold, or sell any securities. Nothing contained herein constitutes tax, legal, insurance, or investment advice. Please consult the appropriate professional regarding your individual circumstance.

Stocks and bonds and commodities are not FDIC insured and can fall in value, and any investment information, securities and commodities mentioned in this report may not be suitable for everyone.

U.S. Treasury bonds and Treasury bills are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return and guaranteed principal value. U.S. government bonds are issued and guaranteed as to the timely payment of principal and interest by the federal government. Treasury bills are certificates reflecting short-term (less than one year) obligations of the U.S. government.

Past performance is not a guarantee of future results.

Different investments involve different degrees of risk, and there can be no assurance that the future performance of any investment, security, commodity or investment strategy that is referenced will be profitable or be suitable for your portfolio.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material.

The information contained is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation.

Before making any investments or making any type of investment decision, please consult with your financial advisor and determine how a security may fit into your investment portfolio, how a decision may affect your financial position and how it may impact your financial goals.

All opinions are subject to change without notice in response to changing market and/or economic conditions.

1 The Dow Jones Industrial Average is an unmanaged index of 30 major companies which cannot be invested into directly. Past performance does not guarantee future results.

2 The NASDAQ Composite is an unmanaged index of companies which cannot be invested into directly. Past performance does not guarantee future results.

3 The S&P 500 Index is an unmanaged index of 500 larger companies which cannot be invested into directly. Past performance does not guarantee future results.

4 The Global Dow is an unmanaged index composed of stocks of 150 top companies. It cannot be invested into directly. Past performance does not guarantee future results.

5 CME Group front-month contract; Prices can and do vary; past performance does not guarantee future results.

6 CME Group continuous contract; Prices can and do vary; past performance does not guarantee future results.